JSTORIES ー In 2022, the Japanese government implemented the "Startup Development Five-year Plan" to increase investment in startups to 10 trillion yen by 2027. According to a report by the Ministry of Economy, Trade, and Industry, one of the key factors necessary for achieving this goal is the promotion of mergers and acquisitions (M&A) and global expansion.

Large corporations like GAFAM have been actively acquiring startups to achieve discontinuous growth. M&As are also seen as a strategic option for stable growth for startups. In fact, in the U.S., 90% of startups choose M&As as their exit strategy instead of an initial public offering (IPO). However, in Japan, there are still relatively few M&As involving startups. Most startups still aim for IPOs, and M&As are not actively utilized as a growth investment strategy.

Why are M&As still underutilized in Japan despite their importance for developing the startup ecosystem alongside international expansion? How can we unlock the potential for business growth through M&As and increase exit options for startups?

To explore these questions, Toshi Maeda, executive editor of J-Stories, interviewed an M&A expert in Japan.

Hidetaka Kojima graduated from the Faculty of Foreign Studies at Tokyo University of Foreign Studies in 2003, completed an MBA from the Graduate School of Commerce and Management at Hitotsubashi University in 2009, and completed the Program for Leadership Development (PLD) at Harvard Business School in 2019.

After working at Daiwa Securities and GCA (now Houlihan Lokey), he joined Mitsubishi Corp. in 2011 to launch the Life Sciences Division and was involved in M&A/PMI. In 2020, he joined SHIFT and established the M&A/PMI system, leading the company’s remarkable M&A results. In 2022, he founded SHIFT Growth Capital and took on the role of Director/CEO of SHIFT USA in 2025 to oversee international strategies. Kojima is also involved as an adviser and angel investor for Japanese startups and aims to build Japan’s startup ecosystem.

SHIFT – The M&A Powerhouse

SHIFT is a company that supports customers in creating "sellable services," with its base in software quality assurance. As of February 2025, the company has about 14,000 employees and 37 group companies. SHIFT aimed for 100 billion yen in sales by 2025 through its midterm growth strategy, "SHIFT1000," and hit this target by the end of fiscal year 2024. SHIFT is now focusing on achieving 300 billion yen in sales through its next strategy, "SHIFT3000," and is implementing various initiatives.

Japan's 'M&A King' examines around 300 deals annually

JStories Executive Editor Toshi Maeda (hereafter, JStories): Today, we have Hidetaka Kojima, the head of M&A/PMI and overseas business development at SHIFT, a company that has maintained remarkable growth in sales over the past decade, specializing in software quality assurance and testing. Kojima-san, we are at SHIFT’s headquarters today, and it’s incredible how close we are to Tokyo Tower!

Hidetaka Kojima (hereafter, Kojima): Yes, everyone who visits here always mentions Tokyo Tower first (laughs). It’s a symbol of Japan, and it’s familiar to both locals and foreigners, so it’s always a good topic of conversation.

JStories: It's truly a fantastic office. In 2023, SHIFT was the Japanese publicly listed company that announced the most M&A deals, making it fair to call you Japan's "M&A King." Today, I'd like to focus on the secrets behind SHIFT's M&A success, which you have been leading.

Kojima: Thank you for having me.

JStories: Our media platform, JStories, has been covering Japanese startups and researchers who have the potential to solve global issues through their technology and services. By distributing this content in multiple languages, we aim to promote Japanese innovation and support the international expansion of Japanese companies.

One area we haven't focused on much until now is startup M&A. However, recently, we've broadened our coverage to include individual startups and the startup ecosystem, which involves cities, venture capital firms, and international players that stimulate innovation. We've been paying attention to startup infrastructure, and I believe M&As are essential to that ecosystem.

Kojima: Absolutely. We've seen a noticeable increase in startup-related M&As in Japan recently. At SHIFT, we evaluate about 300 M&A deals annually, and the proportion involving startups continues to grow. However, compared to overseas markets, it's still relatively low. In the U.S., M&As are the primary exit strategy for startups, but Japan has yet to reach that level.

Today, in addition to discussing SHIFT's M&A/PMI strategies and overseas expansion, I'd love to dive into the challenges facing Japan's startup ecosystem.

JStories: Thank you. Kojima-san, you are definitely the most knowledgeable person when it comes to M&As for Japanese startups. I look forward to hearing your thoughts not only on SHIFT’s M&A/PMI strategy but also on Japan’s startup ecosystem challenges.

SHIFT’s M&A record: the largest number of M&As achieved among Japanese listed companies in 2023

JStories: First, could you tell us about your current role at SHIFT? Since joining the company in 2020 as the head of M&A/PMI, you've built an entire M&A/PMI organization from scratch. In 2022, you also cofounded SHIFT Growth Capital, later becoming its Representative Director in 2024. Additionally, you've recently established SHIFT USA and are overseeing its international business expansion as Director/CEO. That's an impressive track record.

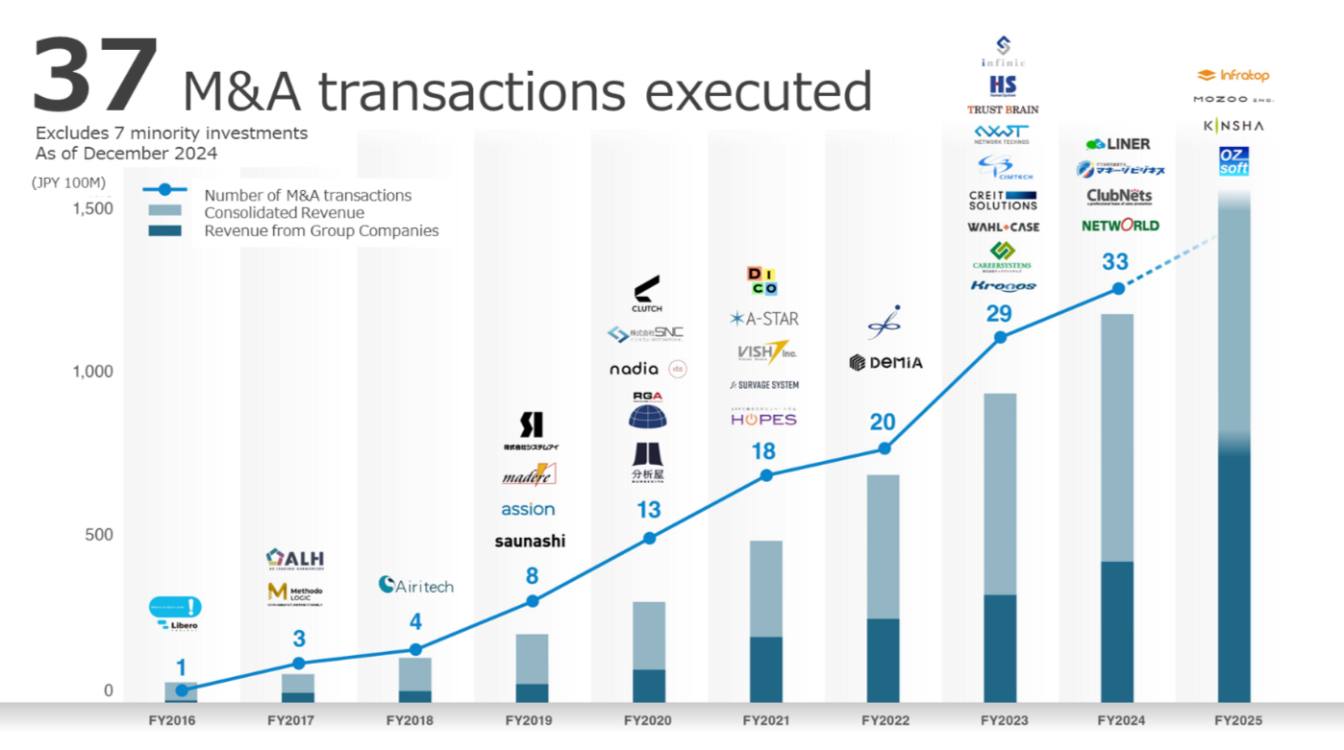

Kojima: SHIFT has conducted around 40 M&A deals so far (excluding capital and business alliances). After establishing our M&A/PMI team in 2020, we have consistently evaluated about 300 potential M&A deals per year. As a result, our group companies have been growing at an average annual rate of 20%-30%.

Recently, more and more people have recognized SHIFT as a company that leverages M&As for rapid business expansion. When speaking with domestic and international investors, I often hear that SHIFT's M&A/PMI strategy is highly repeatable, which strongly validates our approach.

Additionally, we established an overseas team about a year ago. In December last year, we formed business alliances with two U.S. companies. In February this year, we officially launched SHIFT USA. This marks the beginning of our full-scale international expansion, starting with the United States.

JStories: Forty deals — that's an incredible number! Not only has SHIFT executed the highest number of M&A transactions among publicly listed companies in Japan, but your business has also been growing exponentially. It's no exaggeration to call you the M&A King of Japan.

In Japan, M&A deals are far less common than in the U.S. Would you say that SHIFT's approach is unique in this landscape?

Kojima: We constantly monitor disclosed M&A activity, and it’s true that very few companies announce multiple deals every year. I believe there are two major reasons for this: (1) a lack of accumulated M&A/PMI expertise within organizations, and (2) a lack of understanding of the differences in M&A strategies for large enterprises, small and medium-sized businesses (SMEs), and startups.

Regarding the first point, many companies do not have dedicated M&A/PMI teams. Instead, they assemble teams on an ad hoc basis when deals arise, and these teams dissolve once a deal is completed. This makes it difficult to accumulate institutional knowledge about M&As and PMIs. At SHIFT, we have a dedicated M&A/PMI team that has assessed over 1,000 M&A opportunities, allowing us to refine a unique approach. As a result, we can evaluate opportunities more swiftly and execute deals more efficiently, with greater consistency.

Regarding the second point, M&A strategies need to be adjusted depending on whether the target company is a large corporation, an SME, or a startup. Many professionals transition from large corporations to startups and engage in M&As, but those who struggle often fail to recognize these differences. For instance, individuals with a background in large enterprises tend to apply the same M&A methods to startups, which doesn’t work. The reverse is also true. Additionally, M&A transactions involving investment banks differ significantly from those facilitated by intermediaries, even in terms of processes like competitive bidding. It’s essential to understand these nuances and respond accordingly.

JStories: Your expertise in this area is widely recognized, and I hear you receive constant invitations for lectures, seminars, and even offers to serve as an external director or adviser. You've also started teaching regularly at universities, is that correct?

Kojima: Yes, I'm grateful for the opportunities that have come my way. Regarding university lectures, I currently teach courses at Kyoto University for undergraduate students and at the Business School (MBA program).

Last year, I invited Mr. Nakanishi, director of the Industrial Organization Division at Japan's Ministry of Economy, Trade, and Industry (METI), as a guest speaker for a discussion session. METI published the "Guidelines for Corporate Acquisitions" in August 2023, and Mr. Nakanishi was the lead architect of these guidelines.

These guidelines have had a significant impact on "hostile takeovers" in Japan, so our discussion provided valuable insights — from both the policymaker's perspective (who created the guidelines) and the business executive's perspective (who has to implement them).

I hope such conversations will improve Japan's overall M&A literacy and foster a more sophisticated dealmaking environment in the country.

Applying M&A theory and frameworks from investment banking and M&A advisory firms

JStories: Kojima-san, your work in business succession through M&As and increasing the number of unicorn startups is something that Japan urgently needs. However, very few people have the knowledge and expertise you possess. I'd like to understand why you've been able to accomplish things that others haven't. Could you tell us how you first got involved in M&As?

Kojima: I started my career at Daiwa Securities after graduating from university. Later, I transitioned to GCA (now Houlihan Lokey), a boutique M&A advisory firm, where I worked as an M&A adviser for various companies.

While being an adviser provided great learning experiences, I also felt frustrated that I could never truly be on the decision-making side of these deals.

Then, I learned that Mitsubishi Corp. was launching a Life Sciences Division as a model case for business investment, using M&As and PMIs to expand its business. Coincidentally, my graduate school thesis was about how general trading companies should transition into business investment firms, arguing that they should go beyond traditional trading and scale their businesses through investments.

So, when I got the opportunity to join Mitsubishi Corp., I felt it was the perfect environment to take on the challenge I had always wanted. That's when I made the move and began my career in a business corporation.

JStories: So, would it be fair to say that you mastered M&A theory and frameworks at securities firms and M&A advisory firms, then applied them in a trading company to gain practical experience?

Kojima: Yes, exactly. Early in my career, I was exposed to many different corporate M&A strategies as an adviser, and it was an invaluable learning experience. I can confidently say that my fundamental skills in M&A were built during my time as an adviser.

One of the most influential figures in my career was Nobuo Sayama, the founder of GCA and a pioneer of M&As in Japan. Having the chance to work with him had a profound impact on me.

When I transitioned to Mitsubishi Corp. to help establish the Life Sciences Division, I made a commitment to the then Group CEO (who later became Senior Executive Vice President at Mitsubishi Corp.) that we would make this business a core pillar of the company within 10 years.

While my advisory experience helped, I still had much to learn and adapt quickly. Through trial and error, I drove domestic and international M&A and PMI initiatives. After nearly a decade of effort, we successfully turned it into a core business unit.

JStories: So, you set out to make the Life Sciences Division a core part of the company within 10 years — and you did it! Did you feel confident about achieving that goal from the start?

Kojima: I had a clear vision of how to make it happen. I worked backward from the 10-year goal, setting specific milestones along the way. The first five years were focused on strengthening our domestic foundation through M&As and roll-ups. As our business scale grew, we were able to engage in negotiations with global companies on an equal footing. The second half focused on the U.S. market — the largest in the world — where we expanded internationally through acquisitions.

JStories: Despite your success at Mitsubishi Corp., you later joined SHIFT, a venture company. Why did you make this transition?

Kojima: Many people asked me, “Why leave Mitsubishi Corp. for a venture?” (laughs). I had no issues with Mitsubishi Corp., but after achieving my 10-year goal, I wanted a new challenge. Also, I was strongly drawn to SHIFT’s President and CEO, Mr. Tange. After returning from my U.S. assignment, I met with him and discussed SHIFT, its management, M&As, and IT industry challenges. At the end, he said, “Let’s grow SHIFT together!” I was so excited that I immediately accepted his offer.

Joining SHIFT and building a team with like-minded members to achieve top-class M&A performance in Japan

JStories: SHIFT, which you chose as your new challenge, has continued to deliver remarkable results, achieving high revenue growth for the past 10 years. In particular, the company has built a top-class track record in Japan in the field of M&As, which you are responsible for, and as mentioned earlier, has rapidly expanded through these M&A activities. Did you already see a clear path to success before joining?

Kojima: I might sound overconfident, but I saw a path to success (laughs). During my interview with Tange, he asked me about my strengths. I told him: "My biggest strength is my luck — I have always helped every organization I worked for achieve its goals. SHIFT's goals will be realized, too!" I still clearly remember him laughing and saying, "I like that."

Just like I did at Mitsubishi Corp., I worked backward from the company's goals, envisioning the necessary organizational structure, team-building strategies, and initiatives in my mind. After that, all that was left was to put in the effort to prove that my decisions were right.

In 2020, I joined SHIFT and established the Corporate Development Department. The first step was creating two teams under it: the M&A Team and the PMI Team. At first, we had no members, so I focused heavily on recruitment alongside handling daily operations. Compared to now, our track record was still limited, so hiring was quite challenging at the beginning. Fortunately, as time passed, members who resonated with our vision joined us one by one.

Now, we have grown into a structure where three teams — the Strategic Planning Team, M&A Team, and Global Business Development Team — work as one, handling everything from domestic and international M&A strategy formulation to execution, PMI, and global strategy development. The team members come from diverse backgrounds, and I truly believe we have built an incredible team.

JStories: I see. So, by strengthening the team structure, you've been able to accelerate business operations even further?

Kojima: No matter how talented an individual is, they can't scale a business alone. I felt this strongly during my time at Mitsubishi Corp. As M&A activities continue and the organization grows, it becomes impossible for one person to oversee everything. I always think about how to leverage organizational power to scale operations effectively.

For example, in March 2022, to further accelerate our M&A strategy, we established a specialized M&A subsidiary.

JStories: That would be SHIFT Growth Capital, where you serve as the Representative Director, correct?

Kojima: Yes. One of its key features is that as long as we operate within certain predefined criteria (such as investment targets and multiples), decisions can be made by SHIFT Growth Capital's investment committee rather than requiring approval from SHIFT's board of directors. Essentially, a certain level of authority has been delegated from the board. Unlike board meetings, the investment committee can be convened flexibly, significantly speeding up the decision-making process.

PMI strategies for maximizing M&A effectiveness

JStories: You’ve been rapidly growing SHIFT through M&As, haven’t you? I think that M&As are the driving force behind growth, both for Japanese startups and listed companies. How do you view M&As as the driving force for growth?

Kojima: Of course, organic growth is important, and we continue to pursue it. However, I also believe that accelerating growth through M&As — essentially "buying time" — is a necessary strategy.

So far, we've completed around 40 M&A deals, and what matters most is ensuring repeatability. Hitting a home run is great, but it's not something to be praised if it's just a lucky swing. However, consistently hitting base hits every day is praiseworthy. I ensure our team understands this, and we incorporate this mindset into our evaluations. This consistency allows us to execute M&A deals annually and ensures we create value through Post-Merger Integration (PMI).

JStories: You’ve just mentioned PMI, the management integration process. Could you tell us more about it? Essentially, does it mean supporting the acquired companies, sharing SHIFT’s vision and goals, and growing together?

Kojima: Exactly. When a company joins our group, we share SHIFT's vision with them. I use the concepts of "centrifugal force" and "centripetal force" to explain our approach.

In simple terms, we don't micromanage. Still, we encourage acquired companies to fully utilize SHIFT's assets to grow together with us. Rather than imposing changes, we create a structure where group companies can move forward autonomously. As a result, the top-line revenue of our group companies has increased year after year.

JStories: So, to drive business growth, it's not just about closing M&A deals but also about properly executing PMI.

Kojima: Absolutely. To achieve the goals of an M&A and maximize its impact, a well-structured PMI strategy is essential.

As I mentioned earlier, we had no members when we first set up our PMI team. But the team has grown over the past few years, and we've established a structured PMI framework. This has enabled our group companies to sustain an average of 20%-30% annual growth. As a result, group companies now account for about 40% of SHIFT's consolidated revenue.

Of course, we still have challenges ahead. However, since our PMI team consistently adds value to acquired companies, our M&A team can aggressively pursue new deals with full confidence.

JStories: It seems that you’ve built solid teams for both M&As and PMIs. In this context, what do you think is the most important aspect of PMI?

Kojima: I believe there are two main perspectives on PMI. The first is the "100-day plan," which involves ensuring that the minimum required actions are taken in the three months after acquisition. Corporate-related tasks, like fiscal year adjustments and internal controls, are common here, and because the responses are already determined to some extent, it’s easier to standardize this area of PMI. The second is PMI that aims to increase the top line and realize synergy effects. This often requires a case-by-case approach, so it’s not always easy to standardize in detail, but I believe we can standardize it for large themes. In SHIFT’s case, we’ve mainly focused on PMI support requests related to "recruitment," "sales," and "strategy." Recently, we’ve also added "technology" to this. I believe it’s necessary to standardize according to our own resources, stage, and challenges.

End of Part 1.

In Part 2, we will discuss SHIFT’s overseas strategy, the Japanese startup ecosystem, and how to increase unicorns in Japan.

Click here to read the second part of the interview.

***

Translated by JStories (Anita De Michele, Lucas Maltzman)

Edited by Mark Goldsmith

Top video: JStories (Jeremy Touitou, Giulia Righi)

For inquiries regarding this article, please contact jstories@pacificbridge.jp

***

Click here for the Japanese version of the article

_smallthumbnail.jpg)

![[Interview] When digital and physical worlds meet](https://storage.googleapis.com/jstories-cms.appspot.com/images/1747974430456unnamed-2_smallthumbnail.png)

![[Interview] How Japanese musician Grover turned his passion of ‘sound’ into a health-tech startup](https://storage.googleapis.com/jstories-cms.appspot.com/images/1746181078493R7__1407_smallthumbnail.jpg)